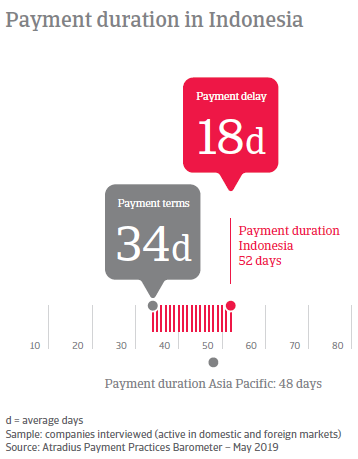

Payment terms extended by survey respondents in Indonesia are notably more relaxed than last year. Does loosing terms on export sales reflect a need to limit the fall off in export demand?

GDP growth in Indonesia, the biggest economy in Southeast Asia, is forecast to remain above 5% in the next two years. Growth will be mainly driven by domestic demand, as export growth will continue to be adversely impacted by lower demand from China (especially for commodities). However, exports account for just 22% of GDP, which makes Indonesia less susceptible to global trade downturns than some other Southeast Asian countries. In any case, the robust domestic sector would moderate the impact.

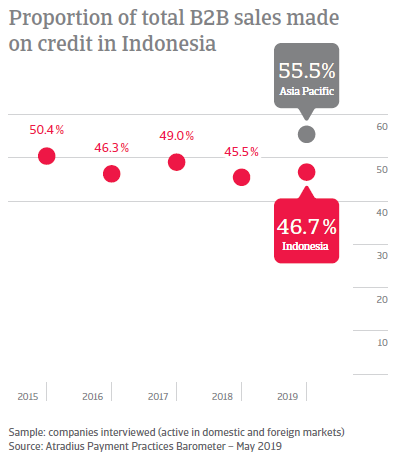

B2B sales on credit increased slightly over the past year, well below the regional average

Current survey data In Indonesia shows a slight increase in the volume of B2B sales made on credit by respondents over the past year (+1.2%, vs. +7.4% at regional level). This amounts to 46.7% of the total value of B2B sales of respondents in the country (up from 45.5% last year). This is well below the 55.5% regional average. On the other hand, 53.3% of the value of B2B sales were made on a cash basis (down from 54.5% one year ago). It is worth noting that, in terms of value of B2B trade on credit, Indonesia ranks third of the countries surveyed in Asia Pacific, after Taiwan (42.8% of credit-based sales) and China (44.3%).

Notably more liberal payment terms to increase export sales

Average payment terms extended by Indonesian respondents to B2B customers appear to be markedly more lenient than one year ago. At 34 days, payment terms in Indonesia were, on average, 11 days longer this year than in last year’s survey. This may reflect a need to loosen terms on export sales, to limit the fall off in export demand. The average terms recorded in Indonesia are near the 32 days average for the region. Only Japan (averaging 41 days), and Taiwan (45 days) have longer average payment terms.

Reserving for bad debts most often used credit management practice

41% of respondents in Indonesia (compared to 33% in Asia Pacific) reported that their credit management policy is chiefly based on reserving against bad debts. Other credit management techniques used more often by Indonesian respondents than by their peers in Asia Pacific are monitoring the payment default risk of their buyers (reported by 34% of respondents in the country vs. 29% at regional level) and requesting secure forms of payment (33% of respondents in Indonesia, compared to 26% in Asia Pacific).

Respondents in Indonesia more likely to take measures to reduce cash outflows then respondents in Asia Pacific overall

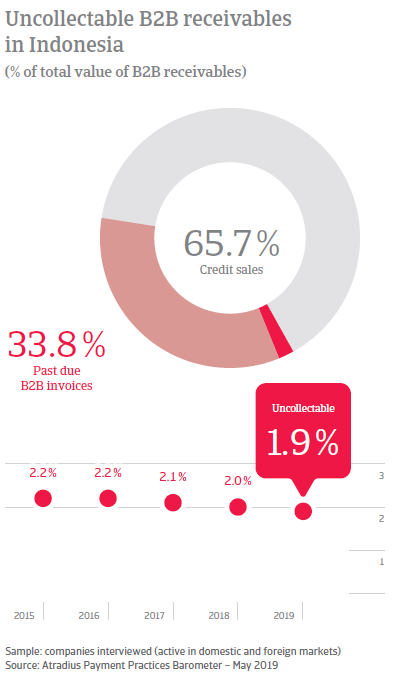

Payment practices of the B2B customers of respondents in Indonesia did not change markedly over the past year. Survey data shows an average of 33.8% of the total value of B2B invoices issued by respondents in the country remained unpaid by the due date (regional average 29.8%). On average, it took Indonesian respondents 3 days longer than the invoiced term to collect past due invoices (no marked change over the past year). In order to avoid liquidity issues caused by late payments by their customers, more respondents in Indonesia (45%) than at regional level (39%) needed to take measures to minimize cash outflows. The corrective measures taken by Indonesian respondents appeared to have a positive effect on the management of uncollectable receivables. Bad debt write offs in Indonesia remained relatively stable at 1.9% of B2B receivables compared to 2.0% last year.

Indonesian respondents more optimistic about future trend in payment practices than their peers in the region

More respondents in Indonesia (45%) than in Asia Pacific overall (25%) appear to be optimistic about the future trends of their B2B customers’ payment practices. 20% of respondents do not expect any change, while 35% anticipate an increase in late payments, as well as in invoices more than 90 days overdue. To protect the business against an increase in the risk of payment default by customers49% of the respondents in Indonesia reported they will request payment from B2B customers in cash or cash equivalents more often over the next 12 months to ensure adequate cash flow levels. Should access to bank financing tighten, 46% said they will take measures to reduce costs.

Overview of payment practices in Indonesia

By business sector

Average payment terms longest in the manufacturing and consumer durables sectors, shortest in the services and construction sectors

Respondents from the Indonesian consumer durables sector extended the longest payment terms to their B2B customers (averaging 39 days from the invoice date). Payment terms in the manufacturing sector followed (38 days). Respondents in the services and the construction sectors set the shortest payment terms, on average (31 days and 24 days respectively).

Being insured against customers’ payment default leaves us free to take advantage of new trade opportunities without worrying about loss of bank funding

Consumer durables sector takes the longest to turn past due invoices into cash

With past due invoices averaging 40.1% of the total value of B2B invoices, the manufacturing sector in Indonesia appears to be the hardest hit by late payments from B2B customers. The agri-food sector follows at 36.5%. At the lower end of the scale, 26.4% of the value of invoices of respondents in the construction sector are past due. The wholesale/retail/distribution sector follows with 29.1%. The average time it takes to convert past due invoices into cash ranges from 57 days from the invoice date in the consumer durables sector to 31 days in the services sector.

Uncollectable receivables highest in the construction and lowest in the services sector

The construction sector in Indonesia recorded the highest proportion of bad debts written off as uncollectable (3.0%), followed by the manufacturing sector at 2.3%. At the lower end of the scale, the services sector wrote off 1.4% of its B2B receivables as uncollectable.

By business size

Micro-enterprises extended the most relaxed payment terms to B2B customers

Respondents from micro-enterprises in Indonesia offered their B2B customers the most relaxed payment terms, averaging 37 days from the invoice date. Payment terms extended by respondents from both SMEs and large enterprises are shorter, averaging 32 days.

Large enterprises recorded an increase in invoices paid late from B2B customers

Micro-enterprises in Indonesia recorded the highest increase in the proportion of B2B invoices paid on time (+8% on average) over the past year. As a result, overdue invoices now account for 31.2% of the total value of B2B invoices in this business size segment. In contrast, large enterprises in Indonesia experienced a 9% increase in past due B2B invoices, on average, over the past year raising the value of overdue invoices to 33% of the total value of invoices. The average time it takes to convert overdue invoices into cash ranges from 56 days from the invoice date for micro-enterprises to 48 days for SMEs.

Large enterprises recorded the highest rate of uncollectable receivables

Large enterprises in Indonesia recorded the highest proportion (2.9%) of B2B receivables written off as uncollectable. The average for SMEs is 2.0% and for micro-enterprises 1.2%.