Atradius Atrium

Portail clients en ligne pour accéder aux informations sur votre contrat et aux outils de gestion de vos limites de crédit.

Termes de recherche populaires

France

France

Allemagne

Allemagne

Australie

Australie

Autriche

Autriche

Belgique

Belgique

Brazil

Brazil

Bulgarie

Bulgarie

Canada

Canada

Chine

Chine

Danemark

Danemark

Émirats arabes unis

Émirats arabes unis

États-Unis

États-Unis

Finlande

France

Finlande

France

Grèce

Grèce

Hong Kong

Hong Kong

Hongrie

Hongrie

Inde

Inde

Irlande

Irlande

Italie

Italie

Japon

Japon

Lituanie

Lituanie

Mexique

Mexique

Norvège

Norvège

Nouvelle-Zélande

Nouvelle-Zélande

Pays-Bas

Pays-Bas

Pologne

Pologne

Portugal

Portugal

République tchèque

République tchèque

Roumanie

Roumanie

Royaume-Uni

Royaume-Uni

Singapour

Singapour

Slovaquie

Slovaquie

Slovénie

Slovénie

Spain

Spain

Suède

Suède

Suisse

Suisse

Turquie

Turquie

Les entreprises britanniques continuent de recourir au crédit commercial avec prudence dans un environnement économique fragile, marqué par des coûts de financement élevés, une demande irrégulière et des pressions persistantes sur les coûts. Environ 68 % des ventes B2B sont réalisées à crédit, un niveau en hausse au cours des derniers mois et désormais supérieur de 16 points de pourcentage à la moyenne d’Europe occidentale. Cet écart reflète une stratégie délibérée des entreprises britanniques, qui cherchent à trouver un équilibre entre le soutien à la croissance de leur activité et la maîtrise du risque. Les décisions relatives au crédit commercial sont influencées par un environnement économique et commercial volatil, dans un contexte de fortes incertitudes géopolitiques et d’affaiblissement de la demande mondiale. Malgré le ralentissement de l’inflation, les conditions de trésorerie demeurent tendues et les pressions sur les coûts restent significatives. Les défaillances d’entreprises se maintiennent à un niveau élevé au Royaume-Uni, en particulier parmi les petites entreprises des secteurs de la construction, du commerce et des activités tournées vers les consommateurs. Le risque lié aux défaillances des clients s’est ainsi renforcé.

Dans ce contexte difficile, la majorité des entreprises britanniques continuent de fixer leurs délais de paiement autour de 30 jours. Toutefois, elles sont beaucoup moins enclines que leurs homologues d’Europe occidentale à accorder des délais plus longs, les prolongations restant relativement rares. Le crédit commercial demeure donc étroitement encadré au Royaume-Uni, les entreprises privilégiant la maîtrise de leur exposition au risque plutôt que l’acceptation de risques structurels supplémentaires.

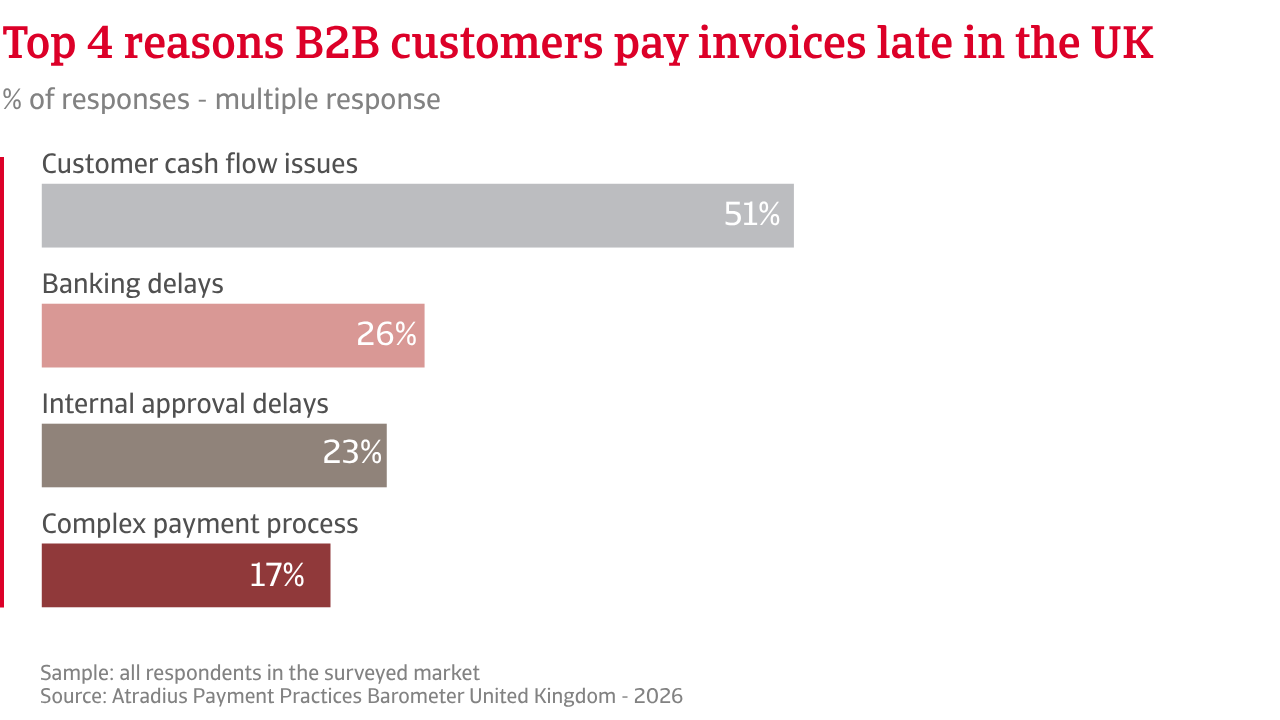

Les retards de paiement restent un enjeu important au Royaume-Uni, même s’ils sont moins fréquents qu’en Europe occidentale. Environ deux tiers des entreprises britanniques déclarent subir des retards de paiement de la part de leurs clients B2B, contre plus de trois quarts à l’échelle régionale. Ces retards concernent près de 25 % du chiffre d’affaires B2B facturé au Royaume-Uni, un niveau légèrement inférieur à la moyenne d’Europe occidentale. Les entreprises britanniques parviennent généralement à encaisser leurs créances plus rapidement que leurs homologues européennes, ce qui se traduit par un délai moyen de recouvrement des créances clients (DSO) plus faible. Toutefois, lorsqu’un retard de paiement survient au Royaume-Uni, il est plus susceptible de se prolonger sur une longue période. Les entreprises britanniques enregistrent des pertes sur créances irrécouvrables pouvant atteindre 2 % du montant des factures B2B, principalement en raison des défaillances de leurs clients. À l’inverse, en Europe occidentale, les retards sont plus fréquents aux stades intermédiaires du recouvrement, mais les retards très longs sont moins courants. Il en résulte un profil de risque différent plutôt qu’un niveau de risque inférieur.

L’impact de ces comportements de paiement sur le besoin en fonds de roulement diffère également. Notre enquête montre que les entreprises d’Europe occidentale sont beaucoup plus nombreuses à réduire leurs investissements de croissance ou d’innovation en réaction directe aux retards de paiement. Le recours au financement externe suit une tendance similaire, avec une proportion nettement plus élevée d’entreprises européennes déclarant une dépendance accrue à des financements tiers. Si les tensions sur le fonds de roulement existent également au Royaume-Uni, elles y demeurent moins généralisées.

Les entreprises britanniques continuent de s’appuyer largement sur une gestion active du risque client pour maîtriser le risque de paiement. Cette approche comprend notamment un suivi étroit des clients, l’utilisation de relances numériques et la mise en place d’incitations au paiement anticipé. L’assurance-crédit joue également un rôle, mais elle est moins largement utilisée qu’en Europe occidentale, où les entreprises combinent plus fréquemment les dispositifs de contrôle interne avec des solutions de transfert du risque.

La plupart des entreprises britanniques continuent de fixer leurs délais de paiement à environ 30 jours. Elles sont bien moins enclines que leurs homologues d'Europe occidentale à passer de délais courts à des délais plus longs, les prolongations étant relativement rares.

Les entreprises britanniques abordent les prochains mois sans véritable dynamique de reprise et dans un contexte de pressions croissantes. Le conflit au Moyen-Orient ajoute un choc énergétique à une économie déjà fragilisée, alimentant les tensions inflationnistes et incitant la Banque d’Angleterre à maintenir une approche prudente. Avec un assouplissement monétaire désormais attendu seulement fin 2026 ou début 2027, les entreprises devront composer plus longtemps avec des coûts de financement élevés. Dans ce contexte, les entreprises n’anticipent que peu d’évolution des comportements de paiement B2B, ce qui reflète davantage une attitude d’attentisme qu’un regain de confiance. Si la majorité des entreprises britanniques ne s’attend à aucun changement notable en matière de paiement B2B, les avis concernant une éventuelle évolution se répartissent de manière équilibrée entre optimisme et prudence. Cette situation contraste avec celle observée en Europe occidentale, où les risques de dégradation dominent les anticipations, traduisant une confiance plus limitée dans les perspectives économiques et commerciales mondiales.

Les résultats de l’enquête montrent que les entreprises britanniques concentrent principalement leurs préoccupations sur les facteurs nationaux, notamment les pressions sur les coûts et les conditions de financement. L’environnement macroéconomique intérieur reste difficile. La croissance demeure modérée, la demande reste fragile et les tensions sur les coûts persistent. L’inflation devrait rester élevée, les coûts d’exploitation demeurent importants et les taux d’intérêt continuent de peser fortement sur l’activité, ce qui maintient des tensions sur le besoin en fonds de roulement. Pour de nombreuses entreprises, cette situation se traduit par une réduction des marges de trésorerie disponibles, alors même que le risque de paiement reste durablement élevé.

Les pressions décrites se reflètent dans les anticipations des entreprises britanniques, qui s’attendent à ce que le niveau actuellement élevé des défaillances d’entreprises se maintienne, au moins à court terme. Les secteurs de la construction et du commerce de gros concentrent la plus forte proportion de défaillances, sous l’effet combiné d’une demande atone, de la hausse des coûts des intrants et de marges structurellement faibles. Une minorité d’entreprises prévoit une augmentation des défaillances, tandis que les autres ne disposent pas d’une visibilité suffisante pour se prononcer clairement. Le manque d’optimisme se retrouve également dans les perspectives de rentabilité. Les entreprises britanniques affichent une confiance plus limitée dans leur capacité à préserver leurs marges. Les préoccupations liées à leur érosion sont nettement plus marquées qu’en Europe occidentale. Avec des marges de manœuvre financières réduites, les entreprises disposent de moins de capacité pour absorber les retards de paiement ou les impayés. À l’inverse, les entreprises d’Europe occidentale semblent mieux positionnées pour faire face à ces difficultés, malgré des perspectives de croissance elles aussi modérées.

Au Royaume-Uni comme en Europe occidentale, les entreprises considèrent la conjoncture économique comme le principal facteur de risque pour les paiements B2B. Les entreprises britanniques se montrent toutefois davantage préoccupées par l’inflation des coûts, les tensions liées au financement et les ralentissements touchant certains secteurs d’activité. Cette situation est cohérente avec la concentration des défaillances observée dans la construction et le commerce de gros, révélatrice de tensions au sein du marché intérieur. En Europe occidentale, les entreprises accordent davantage d’importance aux risques géopolitiques et aux facteurs liés aux marchés internationaux. L’exposition aux échanges transfrontaliers, l’incertitude réglementaire et l’évolution du commerce mondial occupent une place plus importante dans leurs préoccupations. À l’échelle régionale, le risque de paiement est ainsi davantage associé aux chocs externes qu’aux fragilités économiques nationales.

Pour une vue d’ensemble complète des résultats de l’enquête 2026 pour le Royaume-Uni et l’Europe occidentale, téléchargez le rapport consacré au marché britannique dans la section «Télécharger le document » ci-dessous.

Pour renforcer votre stratégie en matière de credit management, contactez-nous pour garder une longueur d'avance !